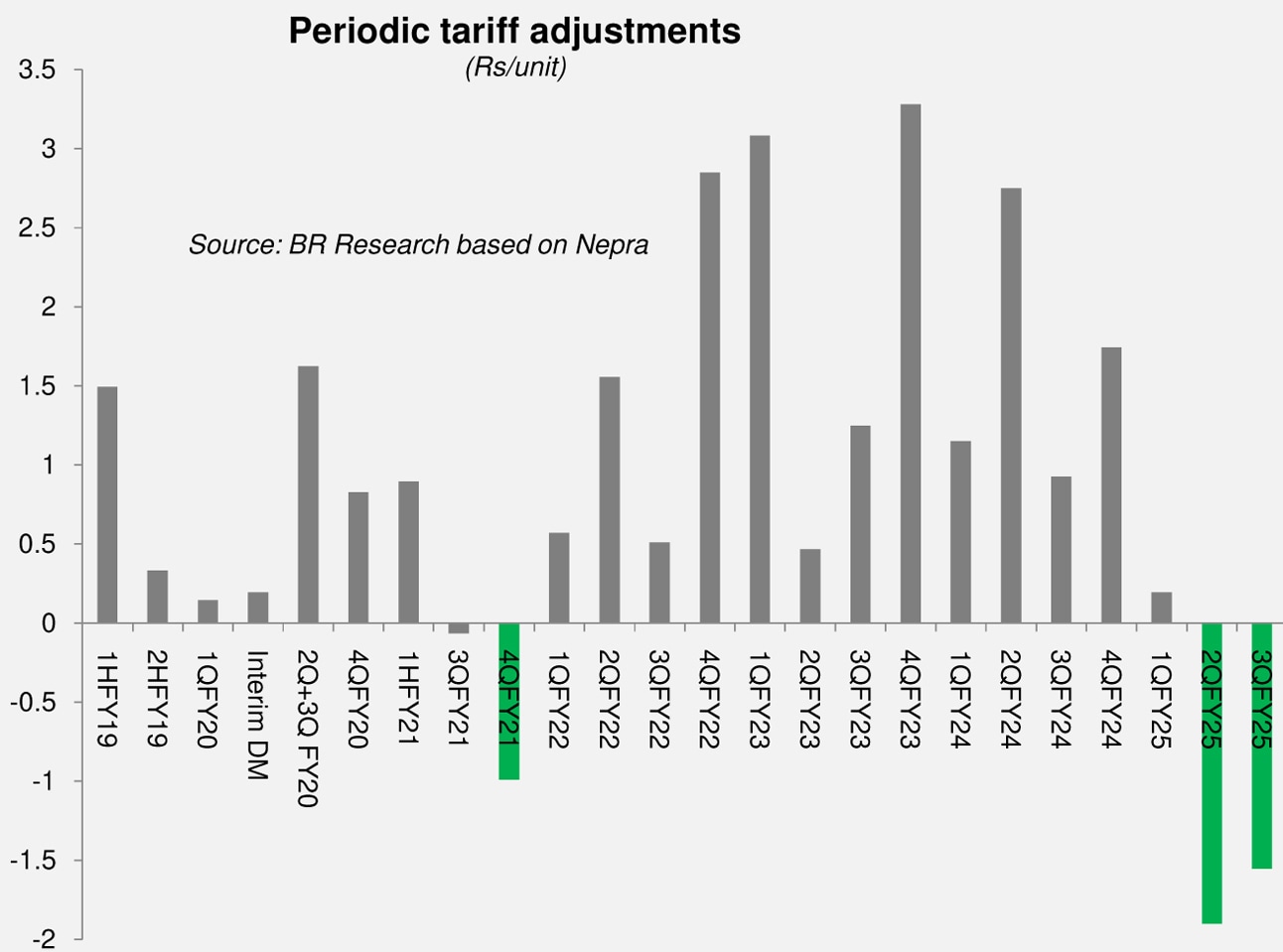

The summer season of massive relief continues for electricity consumers, as another Rs1.55/unit cut in lieu of Quarterly Tariff Adjustment (QTA) has been notified by the regulator.

The QTA for 3QFY25 will be in field for May, June and July 2025.The QTA for May and June will be in addition to the 2QFY25 QTA amounting to Rs1.9/unit – that is already in place till June 2025.

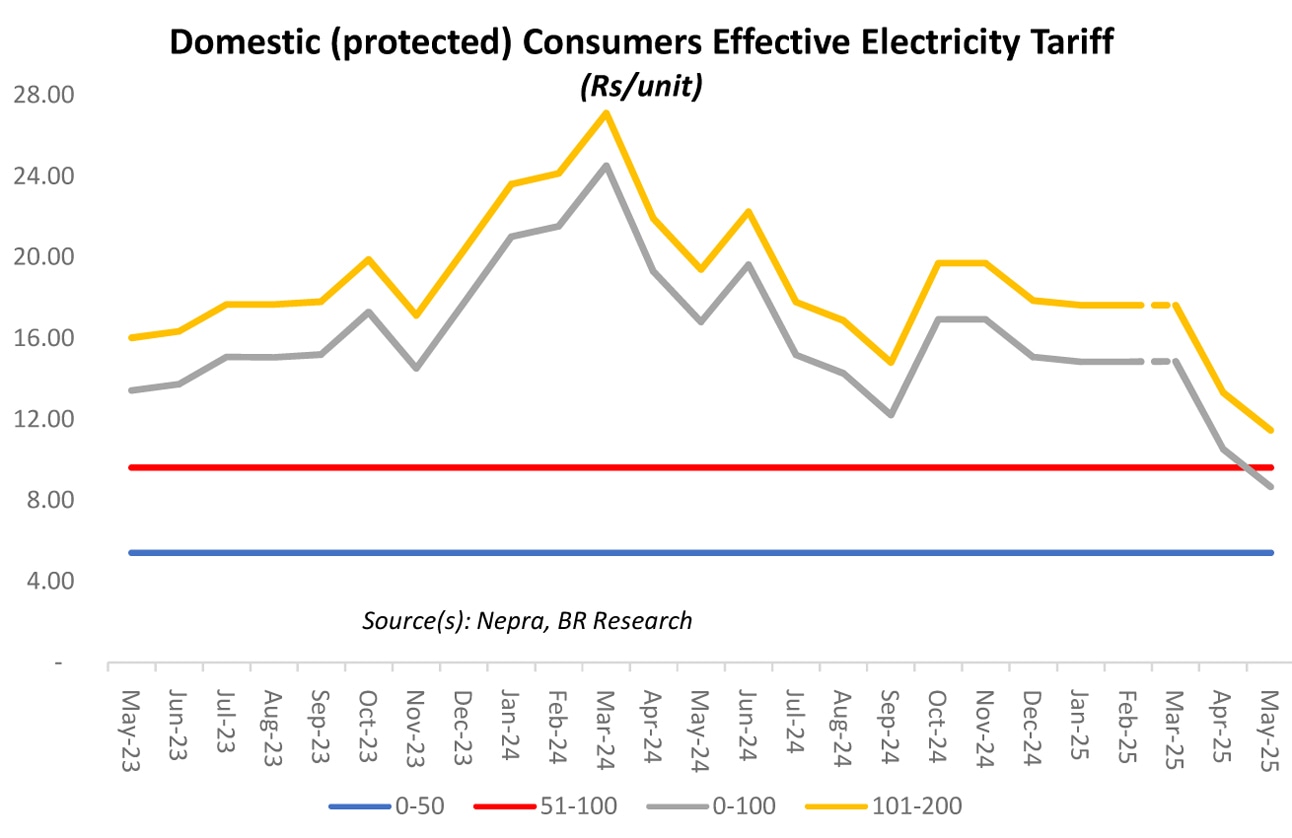

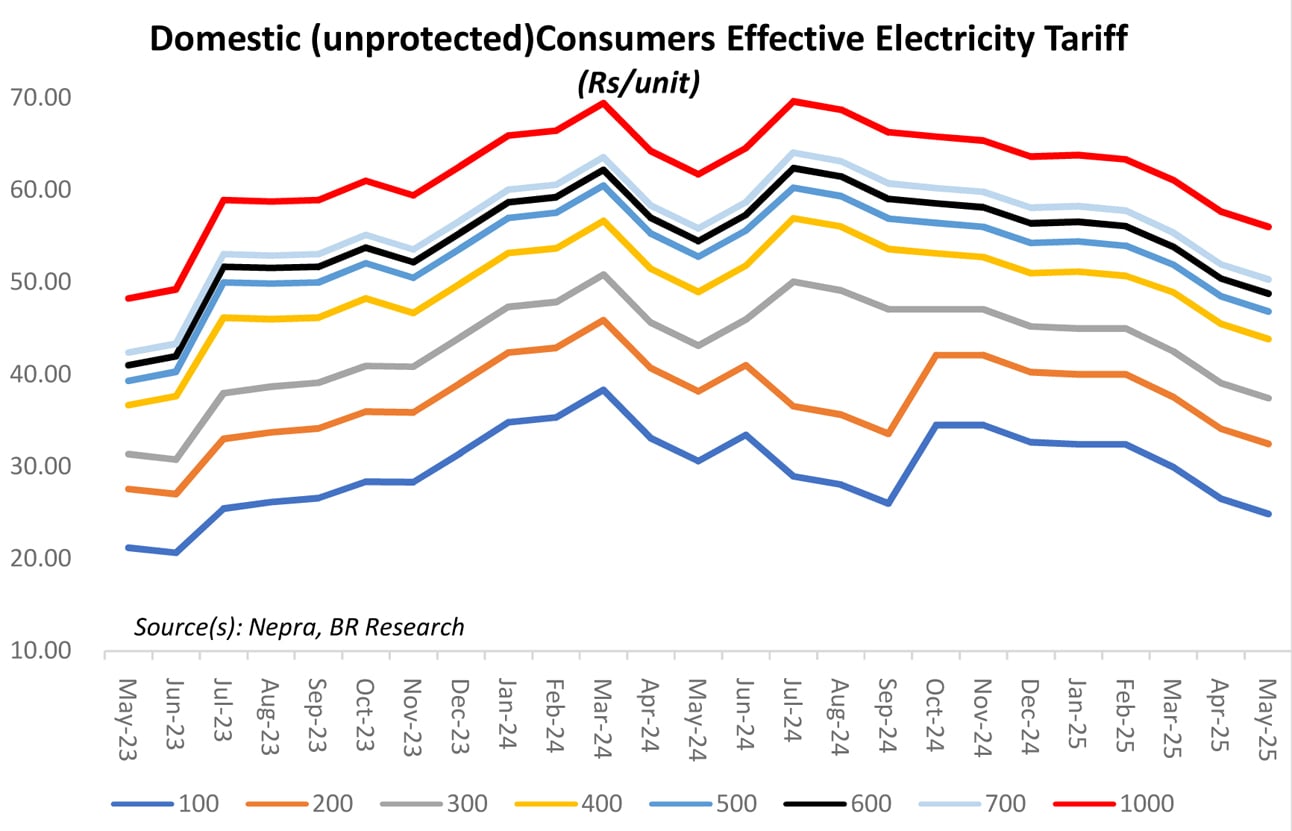

The combined relief over March 2025 now stands at Rs6.2/unit for protected category slabs, and nearly Rs5/unit for unprotected.

The impact includes negative monthly fuel charges adjustment of Rs1.18/per unit, of which Rs0.9 is the temporary adjustment that will last another month. The standalone monthly FCA at Rs0.28/unit for May 2025 is the lowest since September 2024, as deviations with reference generation have increased of late – largely owing to reduced hydrology and increased reliance on RLNG.

The tariff composition has a number of temporary relief heads when compared with March 2025. This is what is in field. Tariff Differential subsidy (TDS) of Rs1.71/unit for April-June, 2QFY25 QTA of negative Rs1.9/unit for Apr-Jun, 3QFY25 QTA of negative Rs1.55/unit for May-July, FCA retention relief of negative Rs0.9/unit for Apr-Jun, and Rs0.28/unit on account of monthly FCA for May 2025. The base tariff, surcharges, duties, and taxes, meanwhile, have remained unchanged.

From a year ago, the tariff respite is rather considerable, ranging from 9 percent to 48 percent across various slabs. Effective tariffs are down Rs8/unit for protected and nearly Rs6/unit for unprotected consumers year-on-year. Interestingly, the effective tariff for the non-lifeline protected consumer in the lowest category is now lower than the lifeline consumer’s highest slab.

The difference is marginal, and temporary – as non-lifeline consumers do not get the benefit of periodic adjustments, which have been rather significant of late.

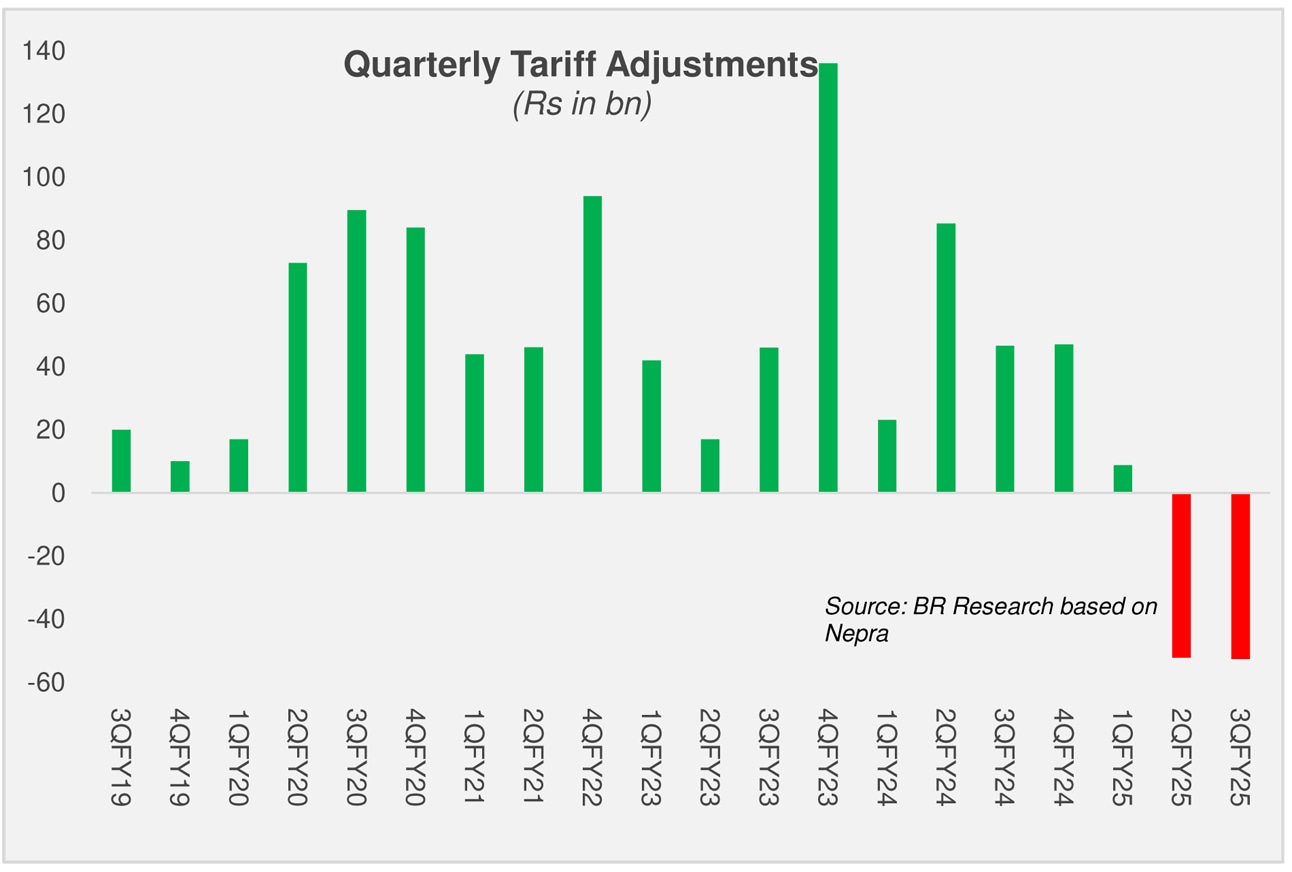

Nearly half of the capacity charges reduction for 3QFY25 stemmed from the impact of termination of 5 plants, and renegotiated terms with a number of IPPs.

A considerable portion owes to the impact of closure of Neelum Jhelum power plant – which may have led to some savings on account of capacity charges but is a net negative for the sector – as no contribution will lead to a visibly altered reference generation mix for the next annual tariff rebasing exercise.

Early signs indicate FY26 base tariffs will be a tad lower or at pat with FY25, and periodic adjustments are expected to be much lower, given the impact of IPP negotiations and terminated contracts will likely be built in the revised Power Purchase Price (PPP) for FY26. All eyes are now on the hydel flows which will be key in keeping power tariffs within close proximity of base tariffs for FY26.

Reference Link:- https://www.brecorder.com/news/40362341